Whether you are materialistic, idealistic, anti-capitalistic or live off-the-grid, you need money. As long as you are human and live on planet earth, you need money.

Talking about money may not be your thing. Too bad, get over it. Like other areas of health, not tending to your finances is a formula for unhappiness which will only worsen with age.

Soooo…, to make this more fun, imagine you are a squirrel. You need to collect nuts ( money) to live on today and store away for winter ( your retirement). To survive through winter, you need to gather more nuts than you need to live on during spring, summer and fall. The following are the habits you need to develop to make this successful.

Let's Get Started:

Pay your Future First

- You, squirrel, have found a job where you are paid in nuts. You get your first nut cheque and immediately stash 10% of your nuts away for winter. You put them in a place where you can’t touch them and learn to live on the remaining 90% until your next cheque. If you have student loans or unfortunately borrowed nuts to buy yourself depreciating assets such as clothes, cars and trips, then use the 10% saved nuts to pay those loans off first. No sense in putting away two nuts per month when your loan sharks are charging you three nuts/per month in interest. You will never get ahead.

Make a Budget and Stick to it

How do you know how much nuts you need to live on monthly? There are cell phone costs, utilities, rent/mortgage, food, entertainment, clothes, transportation and unexpected dental or medical emergencies. You need to make a realistic and detailed spreadsheet of your monthly expenses to avoid going into debt. Why? Because we all underestimate our cost of living.

Yes, it’s a lot of work, but so is working until you are 65, 75, or 85 because you overspent and didn’t save. The one sort of fun part of doing a budget is you get to focus on what is important to you. That morning Starbuck’s coffee or an occasional weekend getaway makes life worth living? Great, put that in the budget. Then figure out which living expense you will scale back on to balance the budget. Maybe cut the clothing budget by buying second-hand? You get to save money and do your bit for the environment. Maybe grow some veggies on your patio or do more home cooking. How about taking your date for a walk, or whatever, in nature, instead of blowing half your pay cheque on fine wine and unhealthy food at an overpriced restaurant? Your budget, your choices. The only rule is that your income is equal to your expenses. The details are for you to decide.

Make your Money Work for You

Suppose you took one nut (yes, we are back to being a squirrel), and we plant that nut. By winter, that nut has grown into a nut tree and produces ten nuts. That is making your nuts work for you! Let’s use a human example. Suppose you put $40,000 into buying a depreciating asset such as a brand-new car. As soon as you drive it off the lot, it’s likely now depreciated to $35,000. In 15 years, it’s worth nothing. In 30 years, it’s still worth nothing. Instead, suppose you put that $40,000 into a fund that holds the top 50 companies in the USA and pays 3% in dividends per year. If you re-invest the dividend, and the market goes up 5% per year on average (well below the 7-8% /year historically), then that $40,000 would have grown to $126,000 in 15 years! In 30 years your investment would be worth $402,000! Amazing how wealth grows if we spend our hard-earned money on appreciating vs depreciating assets.

Start Young

The earlier you start saving and investing, the younger you will reach your retirement goals. $5,000 invested at age 20 in the above fund is worth $160,000 at age 65. You would need to put in $50,000 at age 50 or $100,000 at age 60 to get that $160,000. That is the beauty of compounding and time.

Know the Difference between Gambling and Investing

Someone gives you a tip on this hot tech stock just about to go public. You take your saved money and go all in. That is gambling! Or, you want to learn how to manage your funds yourself instead of giving it all to a wealth manager to invest. You read well-known finance books such as the Wealthy Barber, Rich Dad Poor Dad, and The Intelligent Investor. You learn about asset allocation and what all the terms like P/E, PEG, debt to equity ratios etc., mean. You want to invest in a company around for a long time that has grown its dividend for 20 years, even during the 2008 crash. You determine it is a reasonable price based on your research. You buy some shares. 9/11 happens, and the whole market crashes, including your company’s stock. But you did not invest for a quick buck; you invested for your retirement. You don’t panic. You walk away and try to figure out how planes crashing into a building will affect your company in the long run. You can’t see any long-term effect, but because you are new to this and need to trust your skills, you buy a little more of your beloved company on sale. That is investing.

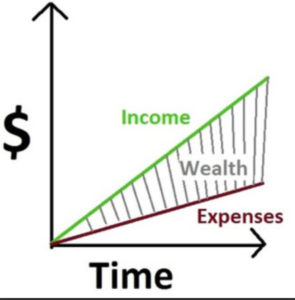

In a nutshell, building wealth is all about living below your means, taking the money you have saved, and making it work for you by buying appreciating assets.

Save it, invest it. It’s that simple.